- If you think you knew why Birmingham City Council went bust, think again.

- Could Birmingham actually un-bust itself overnight (and halt the cuts) at the stroke of the Deputy Prime Minister's pen?

- Did the council unnecessarily hand over almost £0.6 Billion? And could it recover it, and probably even more, back into its revenues immediately, and stop the debilitating cuts?

- Ten charts and four tables tell the story

By Professor John Clancy and Professor David Bailey

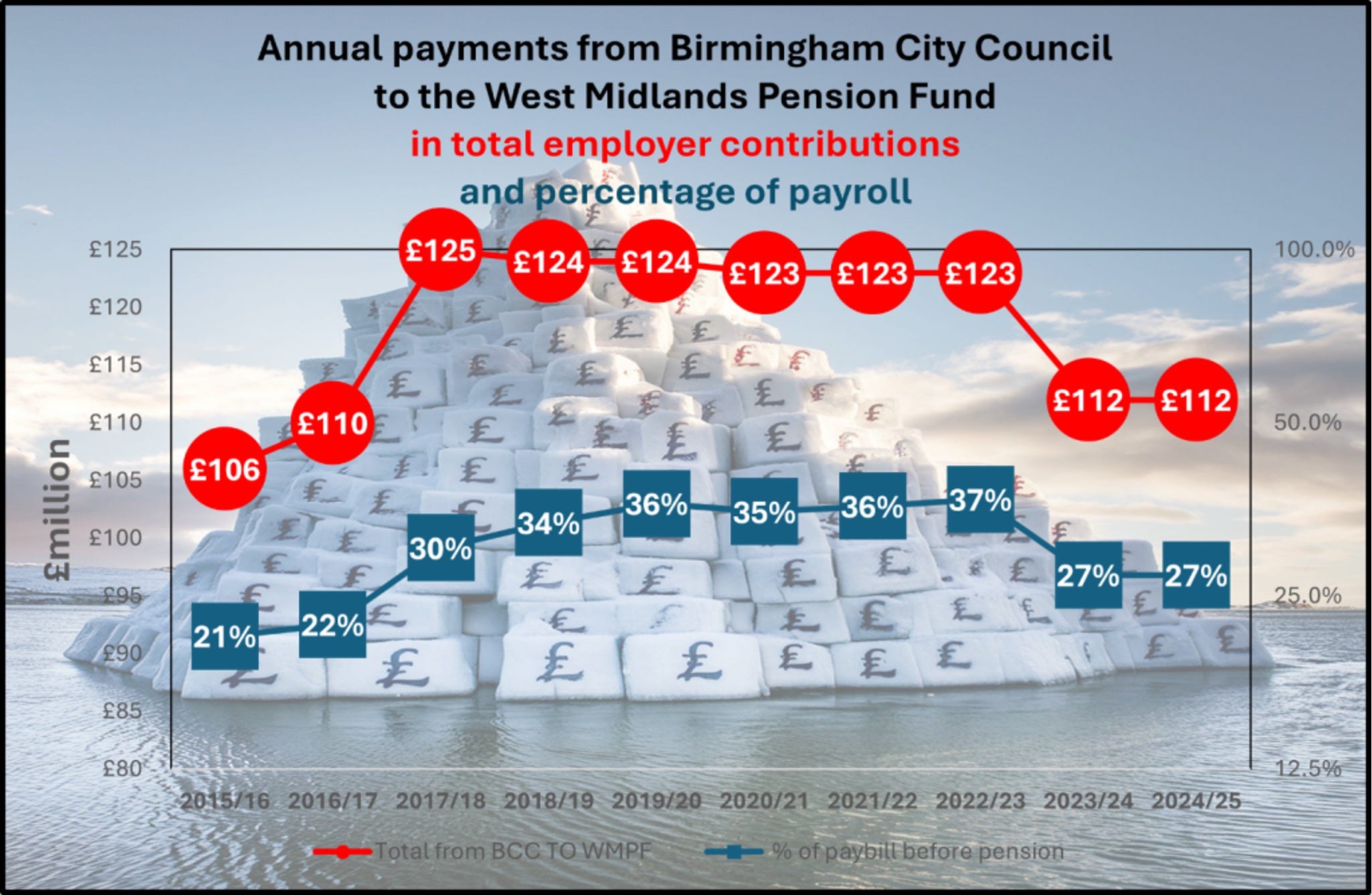

Chart 1 – The Iceberg

Part 1 – The missing half £billion and the lost £1.2 billion

Over the last ten years Birmingham City Council was required by the West Midlands Pension Fund to hand over £1.2 billion pounds to it – in employer's pension contributions. It turns out to have been completely unnecessary.

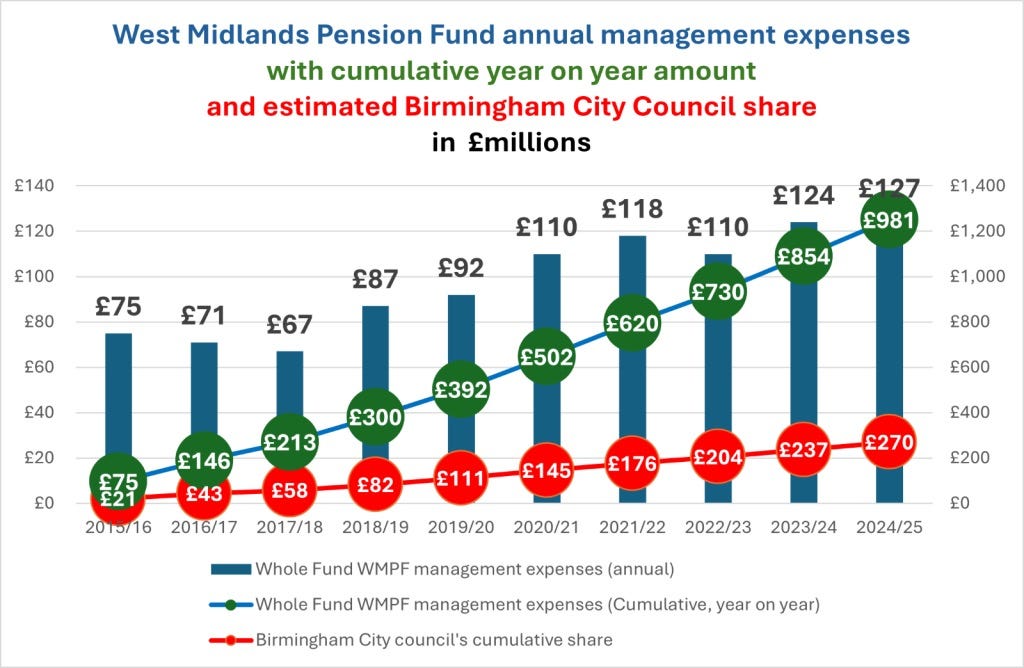

That's bad enough, but over the same period the WMPF perfectly legally deducted from the fund and handed over £1 billion in management expenses.

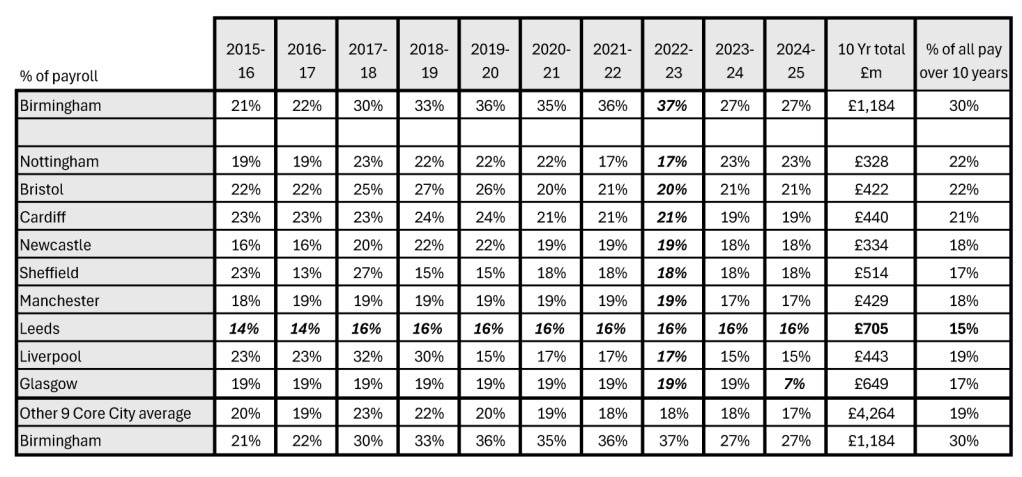

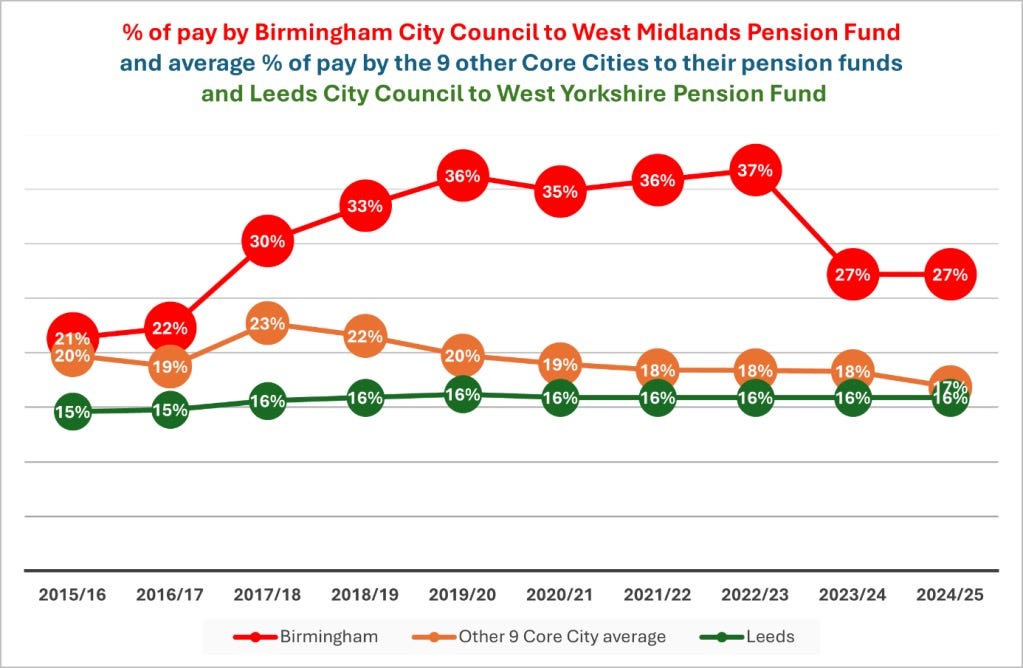

It reached the stage when, by 2022, it was asking Birmingham City Council to pay 37% on top of its standard paybill – to the £20 billion pension fund that runs the ins and outs of pensions for all of the West Midlands councils.

It was literally an extraordinary ask. Birmingham City Council was the only one of the 10 Core City councils in the UK required to pay so much in percentage terms on top of its basic total pay bill. None of the others came anywhere near it.

But Birmingham City Council caved in and paid the bill delivered by WMPF from 2017, again and again, seemingly without question. They shouldn't have. And that was the iceberg which ended up sinking Birmingham City Council in 2023. Everything else is a distraction.

In terms of an explanation for the alleged so-called "bankruptcy", forget the now "widely accepted as wildly-overstated" equal pay issue (as the Birmingham Mail puts it). It's "not a real figure", as Birmingham's Chief Commissioner Max Caller puts it: something John Clancy said using exactly the same phraseology back in 2017, not incidentally.

The awfully real figure of the Oracle disaster, whilst a terribly immediate drain on capital and revenue, could have been absorbed.

There should have been headroom of £0.5 billion more in the council's revenue accounts in 2023 when it apparently went bust. It had been paid instead and, again, unnecessarily into the West Midlands Pension Fund.

The £20 Billion West Midlands Pension Fund pays an average annual pension of little more than £4,900 (and mostly and modally much less). Yet whilst demanding that £1.2 billion from Birmingham City Council, as mentioned earlier, in addition it quite legally deducted from the fund and handed over £1 billion in management expenses over the same period, almost entirely in investment management fees.

From the pockets of Brummies straight into the pockets (almost entirely) of already uber-wealthy London, American and international investment management companies; whilst the council sank into the abyss. Wall Street, not Broad Street.

How much was Birmingham paying out for the management expenses of the fund?

On the basis that Birmingham City Council pays around 28% of WMPF'S administration expenses, we can estimate that Birmingham effectively became responsible for paying £270 million of those management expenses.

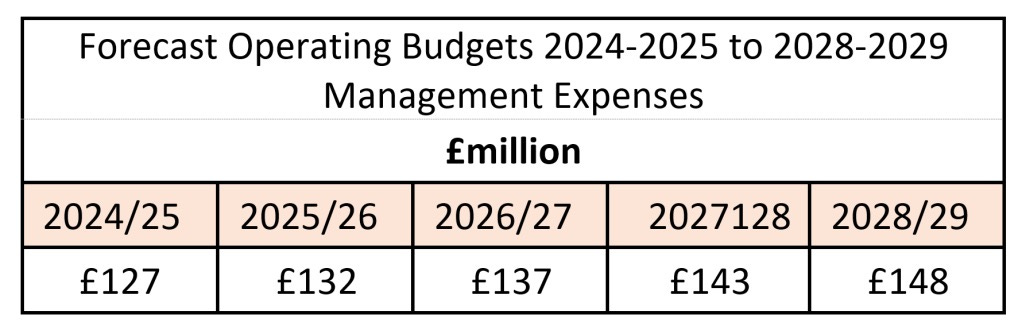

And what of the future for WMPF's management expenses? Here's a table from the 2023 annual report:

So just nearly £0.7 billion over this and the next four years! Time, surely, to step on the brakes and stop those plans.

A Tale of Two Cities

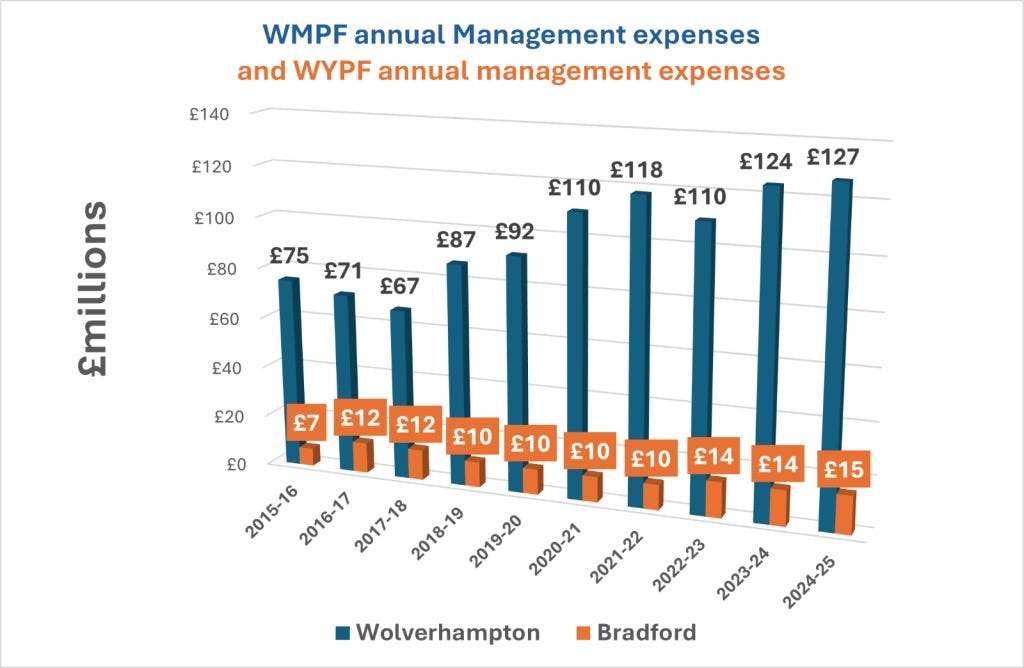

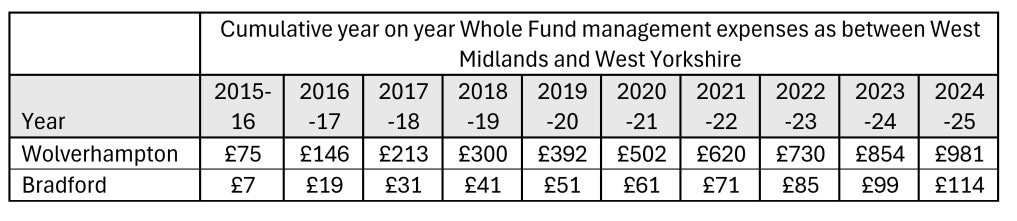

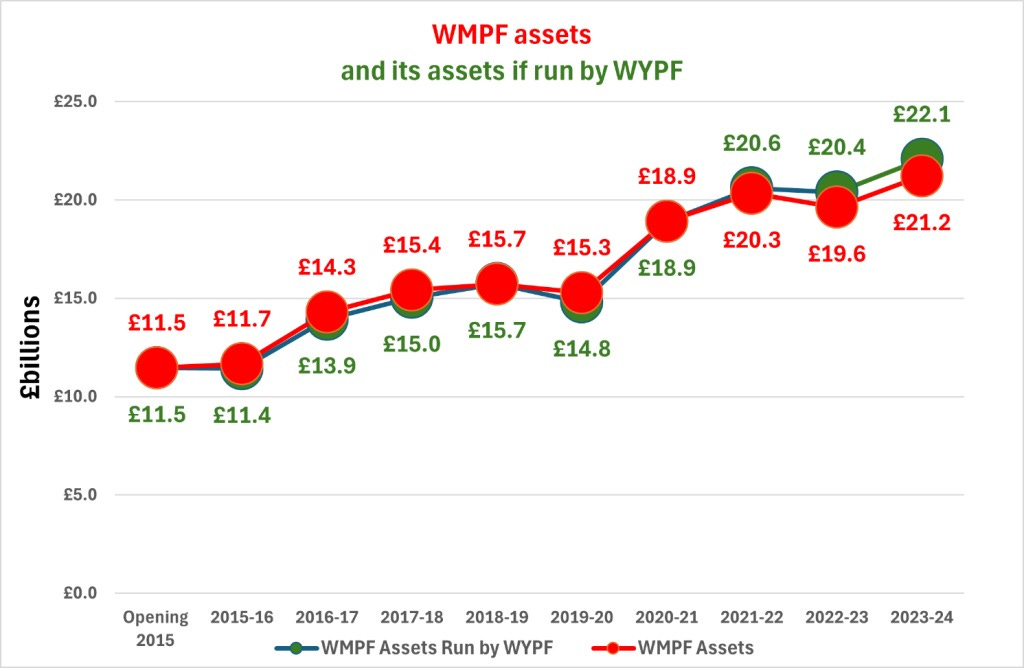

Helpfully, in 2016 the West Yorkshire Pension Fund's size in assets was £11.3 billion. The West Midlands fund was £11.4 billion.

Helpfully also, are the facts that employee contributions in the West Midlands in 2016 were £110.1m, and employee contributions in West Yorkshire were £110.0m. So a highly directly-comparable fund. Like WMPF it has a big city in it – Leeds (the UK's second biggest local council after Birmingham). As WMPF is run by Wolverhampton City Council, so WYPF is run by Bradford City Council

How much would it have cost for Bradford to run the assets and administration of the West Midlands pension fund, instead of Wolverhampton?

Surely for this kind of money the pension fund must have been receiving spectacular returns? And Bradford, not so much?

Not a bit of it.

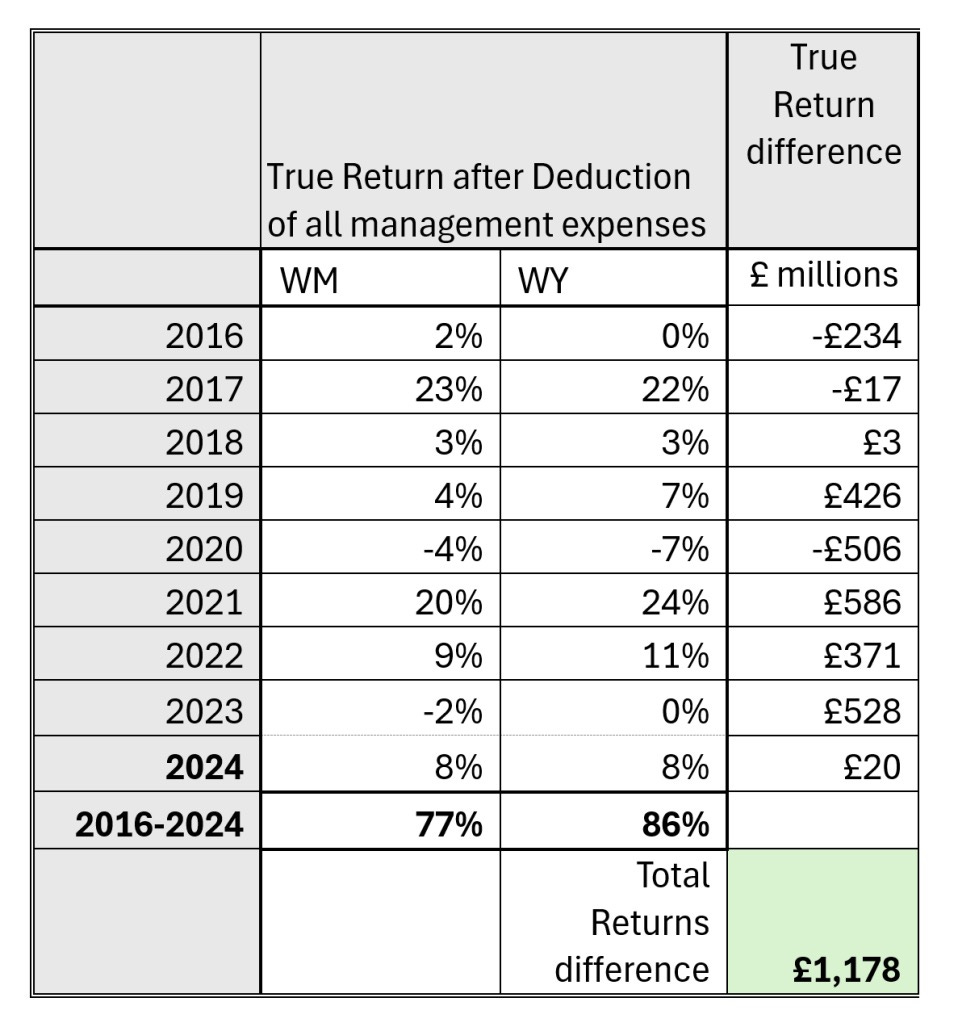

In fact Bradford's in house investment management team outperformed the top external investment managers at the West Midlands fund by 9% points over the 10 years.

Had Bradford invested the assets of the West Midlands fund instead of Wolverhampton, then £1.1 billion more would have been in the West Midlands fund.

If we look at the returns when investment management fees and other management expenses are deducted you get what we would call the True Rate of Return on investments.

So with the unnecessarily massive employers' contributions required by the WMPF, Bradford would have done better running the WMPF assets, anyway.

Where we would be if the employer's contributions had been more than halved to the levels of contributions asked by WYPF of Leeds? Surely there would be less in the fund to invest, so the returns would be massively less? Not much of a difference, either. Wolverhampton asked for £5 billion in employers' contributions; Bradford would have asked for £3 billion and still nearly matched the assets after 10 years.

If Bradford had run the fund there would been 92% of WMPF'S assets today in the fund.

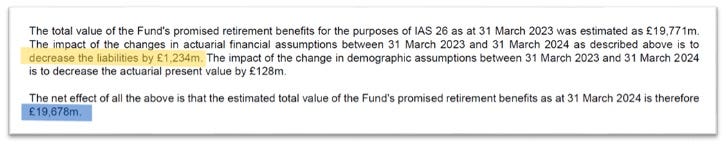

That £19.626 billion for 2024 would, remarkably, have almost exactly matched the international accounting standard liabilities reported just last week in the WMPF Annual Report for March 31st2024 of £19.678 billion:

West Midlands employers would have had £2 billion still in their revenues.

So Bradford would have got it just right. How good do they look right now?

How embarrassing does WMPF look right now?

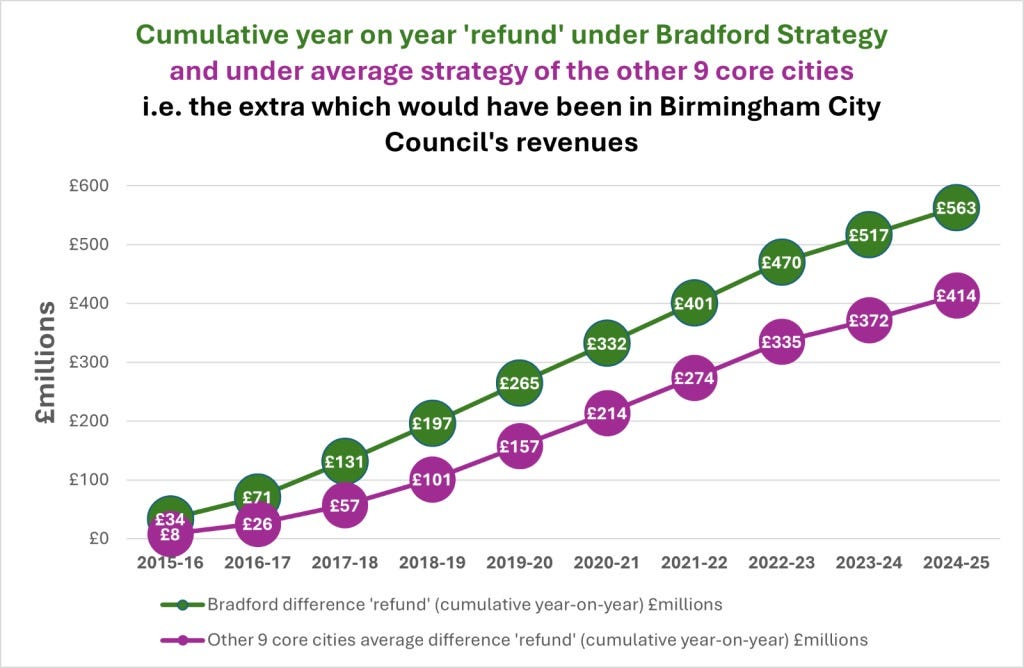

Birmingham would have paid £547 million pounds less in employer contributions, and this would be in the Council's revenue accounts. And in summer 2023, £470 million more would have been in the accounts.

Birmingham would not have 'gone bust'.

How much should Birmingham claim back?

You'll see that this year Glasgow is only paying 7% of its pay bill in employer contributions to its pension fund (the 2nd biggest local government pension fund in the UK), whilst Birmingham is paying 27%. That is because The Local Government Pension Fund Regulationsactually have a regularly-used mechanism to refund what turn out to be overpayments. Glasgow is getting its refund this way, and so should Birmingham

The Glasgow route could be what gets Birmingham out of its mess. And if the WMPF won't do this immediately, then the Deputy Prime Minister Angela Rayner should be persuaded to direct them to do so. Because she can. And the fund would have to comply.

But first, a summary of how much extra could have been available Birmingham City council's revenues had Bradford run the fund, or just the average required by the regional pension funds of the other 9 core cities.

There was an alternative strategy – which pretty much everywhere other than the West Midlandsfollowed.

We are not suggesting that the West Midlands Pension Fund has done anything legally wrong. If anything it was the leeway given by government and regulators by failing to intervene as a matter of political policy. They chose not to bring them to heel. This was simply laissez-faire.

What the managers did do, though, was a subjective choice, and so is subject to challenge. And we challenge it. The managers of the fund were at best utterly naïve in the practical relevance of what turned out to be their mistaken calculations.

There was no real deficit, it was entirely notional – now there's a stonking great surplus

In his blog for the Centre for Brexit Studies at Birmingham City University back in October 2022, John Clancy predicted that the nonsense calculations which were being made by politically naïve actuaries in pension funds of all kinds, private and state, were summoning up illusory deficit calculations. He specifically predicted that very soon pension funds would be reporting surpluses all over the place.

The utterly short-termist, bonkers requirements for increases and overpayments in employers' and employees' contributions would be seen to have been pointless: considerable short-term pain for absolutely no ultimate gain.

And so it came to pass.

And so for one final graph:

All local government pension funds have to comply with International Accounting Standard 26 (IAS26), in reporting annually what the liabilities of the pension fund are, as we saw above in last week's annual report.

They use something called a discount rate which is the most important calculation they use to tell us the effective value today of all the pensions owed to all the present and future pensioners

They substantially use the yield on high quality corporate bonds (AA+ 15+ years) to work out what level of assets the pension fund needs to have todaywhich when added to the likely future investment returns on today's assets, will be able to pay out the future pensions to all of their pensioners, in some cases in over 50 years time.

The thing is, the higher the discount rate, the more of that future debt get chipped away at when dis-counting backwards from all the future pensions.

Think of a bag of 100 ice cubes with pound signs inside each one. If you take out 10 ice cubes every minute, after 5 minutes the bag will be half empty, or half full. If you take out two ice cubes every minute, after the same 5 minutes, there will still be 90 ice cubes in the bag. It will be 90% full, or 10% empty, if you will.

So what happened in pension funds was, because of the financial crash, huge quantitative easing, and near 0% interest rates, discount rates fell to unsustainably low levels for pension funds and they started reporting these huge liabilities.

Had corporate bond rates stayed generally around the long term level of 6% or more, these liabilities would not have been reported. The bag of financial ice cubes would have been almost half full, not almost completely full.

COVID's economic impact, and then oil price hikes, and suddenly high inflation made the whole thing worse. These offset the expected increase in bond rates, so bond prices fell ultra-low. So, for most of the 2010s and then the early 2020s they remained at little more than 2%.

For illustration, you will see from the US 20+YEAR high quality corporate bond graph, that this suddenly changed from the first quarter of 2022. Last year rates hit 6%, and they are currently at 5.4%. Most commentators think they will settle at 6% during the next year.

To remind you, as recently as just 2022 the WMPF was calculating its liabilities using a discount rate of 2%.

Consequently, the WMPF has now has a stonking great surplus – specifically £1.5 billion more in assets than the calculations for all the pensions it will ever have to pay out – to the pensions of its current pensioners and the future pensions of its current employees.

The impact of the change in discount rates reduced the liabilities by £7.5 billion in just one year in 2023from a quite ridiculous £30 billion, and then a further £1.3 billion the following year. Combined with increased asset values, £10 billion was wiped off the liabilities.

The other discount rate used by pension funds was to calculate it not just on corporate bonds, but using an estimated rate of return on the kind of investments the fund had. This was usually much higher and was used for the funding strategy. However these rates suddenly converged in 2023, so there was far less doubt. In fact the IAS26 discount rates suddenly started to look like a much more reliable calculation. The other was just an ever-changing guess.

What Bradford, in particular, and the other 8 core cities' funds did do was not to take a short term view. They judged quite rightly (in a fund which considers 60 years ahead) that in the medium term things would right themselves. And they did. So they did not ask for the kinds of literally extraordinary employers' contributions WMPF did, who effectively assumed these rates would be around for 20 years.

That was the difference, and that's why Birmingham is entitled to get its money back.

Taxi for Mr. Caller?

So the deficit turned out to be, to coin a phrase, "not a real figure".

Talking of which, why didn't the Michael Gove-appointed chief commissioner for Birmingham Max Caller not report the pension fund obvious overpayments and now surplus to Michael Gove? Or wasn't that in the script? Has he reported it to his new boss, the Deputy Prime Minister? More importantly, why hasn't he told the people of Birmingham? Can he prove with evidence that he even knew about it? If he can't, he'll have to go.

Our next two blogs will look at the mechanisms to retrieve these sums back into the council's revenues and ask the questions which need to be asked, and who should answer them; especially the council, its commissioners, its auditors, successive Tory Secretaries of State, senior Whitehall civil servants and the Pensions Regulator. It will also provide a plan of action for immediate next steps for Birmingham and the wider West Midlands employers.

Birmingham's share of the WMPF is approximately 27%. We now predict that when we see this year's BCC annual statement of accounts which reports Birmingham's share there will be a surplus of approaching £1 billion. That assumes that discount rates remain at 5.4%.If corporate bond prices settle at 6% it could be £1.6 billion or more.

The path now Is clear.

It's time for Birmingham to cash out.

.jpg)

Letter to the Deputy Prime Minister

Our letter to the Angela Rayner calling for specific intervention in Birmingham to halt hundreds of £millions of unnecessary further overpayments to its pension fund, and stop £200 million worth of cuts.

Happy New Year from Birmingham City Council - to all our pension fund investment managers!

Birmingham City Council agrees to increase the expenses of its Pension Fund investment managers to £35.5 million a year, or £3 million a month, whilst agreeing massive cuts to services.

Chief Commissioner Caller in the gutter

Unable and unwilling to understand the basics of council pension funds, its Gove-imposed Chief commissioner resorts to insults, and enforces cuts whilst ignoring hundreds of £millions due back from the pension fund.

Here's one they made earlier: how pension funds return surpluses to their councils

Stop dithering, Birmingham. Come clean, Max Caller.

How long will it take Max Caller, the Chief Commissioner of Birmingham City Council, to confirm that the pension fund surplus reported last March in the City Council accounts was £417million?

The calculations have been done and the facts are before him, but Gove's chief commissioner refuses to publish the figure. We know what it is, he knows what it is - why won't he tell the people of Birmingham what it is?

John Clancy and David Bailey

John Clancy and David Bailey